Insurance AI Claims Automation: Faster Processing and Better Accuracy

- eCommerce AI Expert

- Apr 28

- 6 min read

A claim is the test of an insurance promise. Every policy is a commitment — that when the insured event occurs, the insurer will respond quickly, fairly, and competently. The claims process is where that commitment is either honoured or revealed as inadequate. And across most of the insurance industry, the claims process has historically been the point where the gap between the promise and the experience is widest.

Processing delays, documentation complexity, opaque decision-making, inconsistent outcomes for similar claims, and the friction of a process that requires the policyholder to expend significant effort at their moment of maximum stress — these are the characteristics that have defined the claims experience for most customers. They are not design choices. They are the accumulated consequence of a manual process that was never designed for the volume, variety, and speed expectations of modern insurance customers.

AI claims automation addresses this gap systematically. Not by removing the human judgment that genuinely complex claims require, but by automating the processing steps that do not require it — and by providing the intelligence infrastructure that makes the human judgment applied to complex claims more accurate, more consistent, and more defensible. The result is a claims operation that is faster where speed is achievable, more accurate where precision matters, and more consistent across the full claims portfolio.

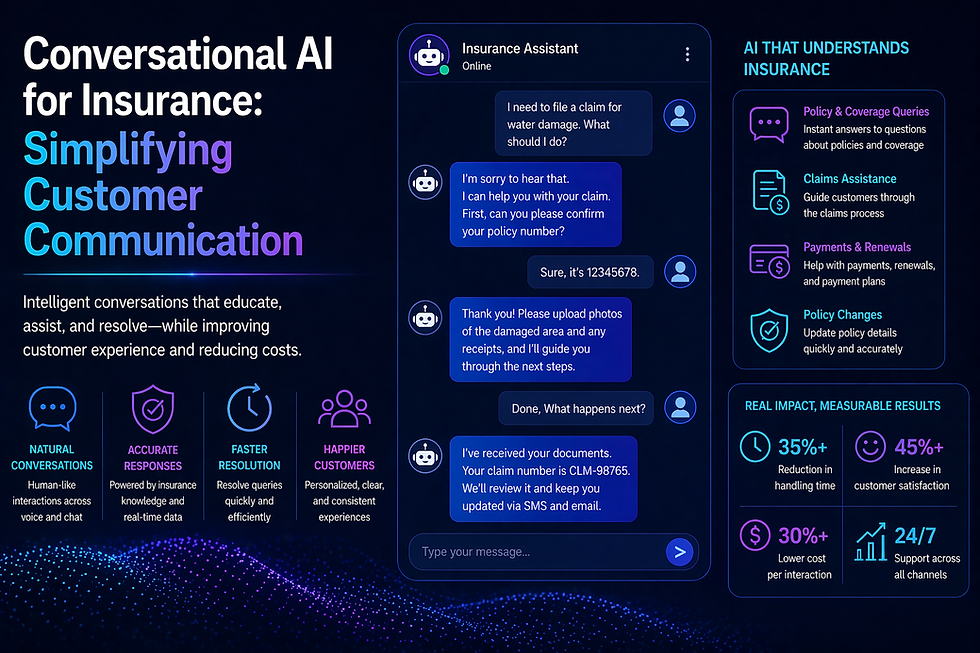

The Claims Processing Steps That AI Automates

First Notice of Loss Capture and Validation

The first contact a claimant makes after an insured event sets the tone for everything that follows. In a manual FNOL process, this contact is constrained by agent availability — the claimant may wait, repeat themselves across multiple channels, or submit information through a form process that is ill-suited to the complexity of what they are trying to communicate.

AI-powered FNOL automation handles initial claim intake immediately, at any time, across any channel. It conducts the intake conversation in natural language — asking the questions the claims team needs answered, in the order that makes the most sense given the claimant's situation, without the rigidity of a structured form. It validates the information provided in real time — checking policy coverage, confirming policy status, verifying the claim details against the policy terms — and identifies the basic eligibility questions that determine whether the claim can proceed before any further resource is committed.

The validation that FNOL automation performs is itself a significant source of speed and accuracy improvement. Claims that enter the processing pipeline already validated against the basic coverage conditions do not require early-stage handler attention to perform that validation manually. The handler who picks up the validated claim begins at a later stage in the process than they would with an unvalidated submission — and the overall cycle time from first notice to resolution compresses accordingly.

Document Collection and Verification

Claims require documentation. Repair estimates, medical records, police reports, property valuations, receipts, photographs — the specific documents required vary by claim type, but the process of collecting and verifying them is universally one of the most time-consuming elements of the claims cycle. Documents arrive late, arrive incomplete, arrive in formats that are difficult to process, or require follow-up to confirm their authenticity.

AI document processing automation changes this step in several ways simultaneously. It extracts relevant information from submitted documents without manual reading — pulling repair costs from an estimate, diagnosis codes from a medical report, or valuation figures from a survey without a handler working through each document individually. It identifies gaps in the documentation and automatically requests the specific missing items rather than waiting for the handler to identify the gap. It validates document authenticity against the patterns that distinguish genuine documents from fabricated ones, flagging anomalies for human review rather than passing them through to settlement.

The combination of faster extraction, proactive gap identification, and automated validation compresses the documentation phase of the claims cycle substantially — often by more than any other single automation intervention, because documentation delays are the most common source of extended cycle times in claims handling.

Coverage Determination and Liability Assessment

For standard claims that fall clearly within or clearly outside the policy coverage, AI systems can perform coverage determination automatically — applying the policy terms and conditions to the circumstances of the claim and producing a clear eligibility finding without handler involvement. This is not a simple lookup. Policy terms are complex, circumstance-specific, and subject to interpretation. AI systems trained on the full policy language and the historical coverage decisions made for comparable claims can apply this complexity with a consistency that manual determination cannot match at volume.

For liability assessment in motor and liability lines, AI systems that process the incident details, third-party information, and available evidence can produce a liability split recommendation that reflects the established legal and actuarial principles applicable to the specific scenario. This recommendation is not the final determination — human judgment applies that — but it provides the starting framework that significantly accelerates the handler's assessment process.

Settlement Calculation and Payment Processing

The settlement calculation for straightforward claims — where coverage is confirmed, damage is documented, and liability is clear — can be automated entirely. AI systems that apply the policy terms, the documented loss, the applicable depreciation or replacement value rules, and any applicable deductibles produce a settlement figure that reflects the correct application of the policy to the circumstances, without the calculation errors that manual settlement computation sometimes introduces.

Payment authorisation and processing for automated settlements can follow immediately — reducing the gap between settlement decision and policyholder receipt from days to hours or minutes. The policyholder who submits a straightforward home contents claim on Monday can receive a validated, calculated, and authorised payment by Tuesday rather than waiting while a handler schedules the calculation and a payment team processes the transfer.

Accuracy: Where AI Outperforms Manual Processing

Speed is the most visible dimension of claims automation improvement. Accuracy is the more commercially significant one — because inaccurate claims processing creates costs in multiple directions simultaneously.

Overpayment — settling claims at amounts above the correctly calculated entitlement — is an immediate financial loss. Underpayment — settling at amounts below correct entitlement — generates complaints, regulatory risk, and the reputational damage of a perception that the insurer is systematically unfair. Inconsistency — settling similar claims at different amounts based on which handler processed them — creates both financial exposure and fairness questions that are difficult to defend when challenged.

AI systems apply the same rules to every claim — consistently, without the variance that comes from handler interpretation differences, workload effects, or the human tendency to apply slightly different standards across different claim profiles. This consistency does not eliminate the legitimate variation that reflects genuine differences between claims. It eliminates the spurious variation that reflects the limits of human attention at volume.

Pattern-Based Accuracy

Beyond consistency, AI systems bring pattern-based accuracy that human handlers cannot provide at scale. A handler reviewing a claim for suspicious indicators draws on their own experience of the fraud patterns they have personally encountered. An AI system draws on the patterns embedded in millions of claims — identifying the combinations of characteristics that have historically preceded fraud or error outcomes with a precision and breadth that individual experience cannot match.

This pattern-based accuracy extends to subrogation opportunity identification — the recognition that a settled claim may have a recovery pathway against a third party — and to the identification of claims where the submitted amount is not consistent with the historical distribution for that loss type in that location. Both represent financial accuracy improvements that are difficult to achieve consistently through manual processing at volume.

The Handler's Role in an Automated Claims Operation

AI claims automation does not replace claims handlers. It changes what they handle. The routine, data-complete, standard-coverage claims that previously consumed the majority of handler time are processed automatically — leaving the human claims team to focus on the cases that genuinely require human judgment: complex liability questions, unusual loss circumstances, customer situations requiring empathy and discretion, fraud investigations that need the intuition and investigative capability that humans bring to ambiguous cases.

This redistribution of work makes the claims team both more efficient and more capable. Handlers who are not spending most of their time processing standard claims have more cognitive bandwidth for the complex cases that reach them. The quality of human judgment applied to complex claims improves when it is not diluted by the volume of routine processing.

Conclusion

Insurance claims automation is the most direct path to the claim experience that policyholders have always deserved — fast, fair, accurate, and transparent. Not because technology removes the difficulty of insurance claims handling, but because it applies the right capability at each step of the process: automation where consistency and speed create value, human judgment where complexity and discretion require it.

The insurers that build this capability are not just improving their operational efficiency. They are honouring the promise that every insurance policy makes — that when the moment comes, the response will be as good as the product that was sold.

A claim handled fast and correctly is the insurance product working as it should. AI is what makes that possible consistently, at scale.

Comments